Buckle in guys, we’re moving into uncharted territory this Christmas retail season. Wuuup wuuup! Sound the alarms! Those ‘unprecedented times’ have left us in some pretty f*cking dire circumstances when it comes to the Global Economy let alone the state of our bank balances 🙃😭.

This all got me thinking about Buy Now, Pay Later providers in the Australian retail industry.

Because it’s probably no surprise that now, more than ever, people are going to be considering payment plans for their purchases at Christmas.

Whilst working on a couple of recent projects I realised that my clients and service providers aren’t completely across of all the options out there when it comes to Buy Now, Pay Later (BNPL). Hint: there is more to life than just AfterPay. So, I thought I’d give you a quick crash course into the wild world of Buy Now Pay Later payment providers and why you can’t afford to ignore them in your retail or e-commerce biz.

What’s more if you don’t take it from me, the banks are listening… which generally means we should too. Last week, NAB and Comm Bank both launched their first interest free credit cards in a drive to try and reclaim dwindling credit card use in customers as they switch to BNPL providers.

“Our data shows that to be competitive, retailers should be exploring new and emerging payment products such as BNPL and mobile and digital wallets to stay relevant in the marketplace.” Phil Pomford, General Manager Global E-commerce at APAC Worldpay Merchant Solutions.

First up a quick stats sesh, because I’m a total data nerd 🤓

-

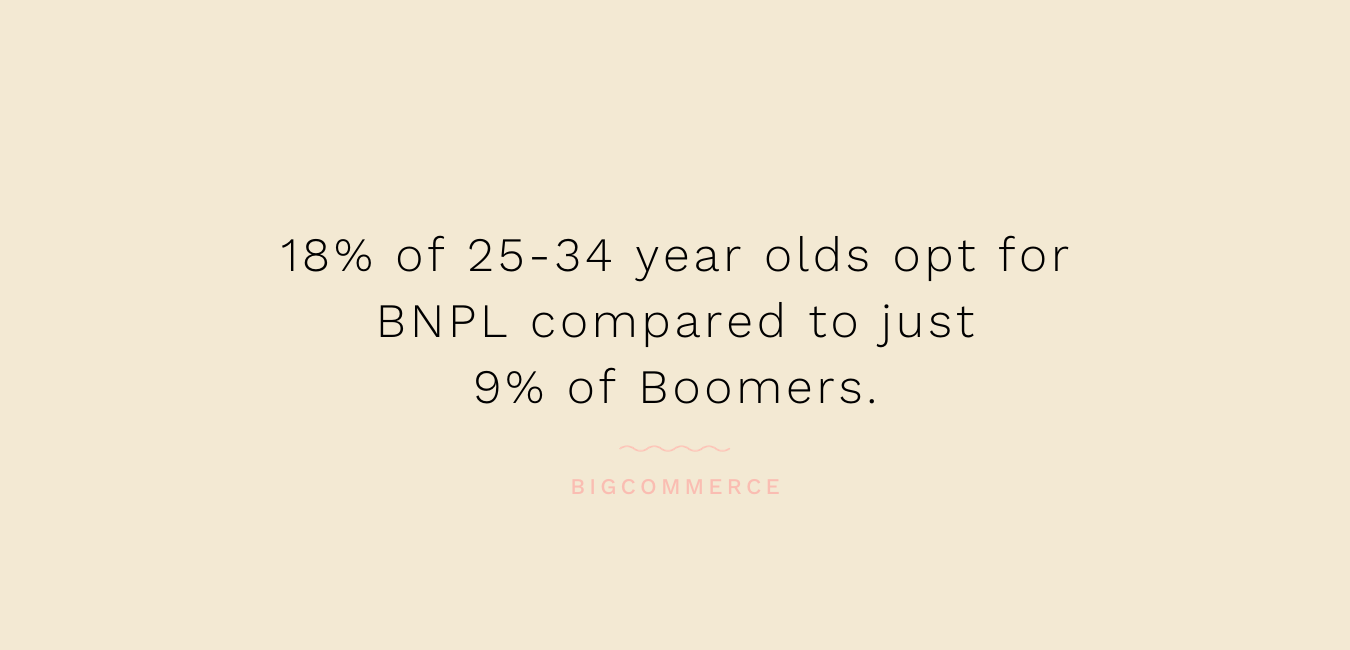

18 percent of 25-34 year olds opt for Buy Now Pay Later as a payment method compared to just 9% of Boomers

-

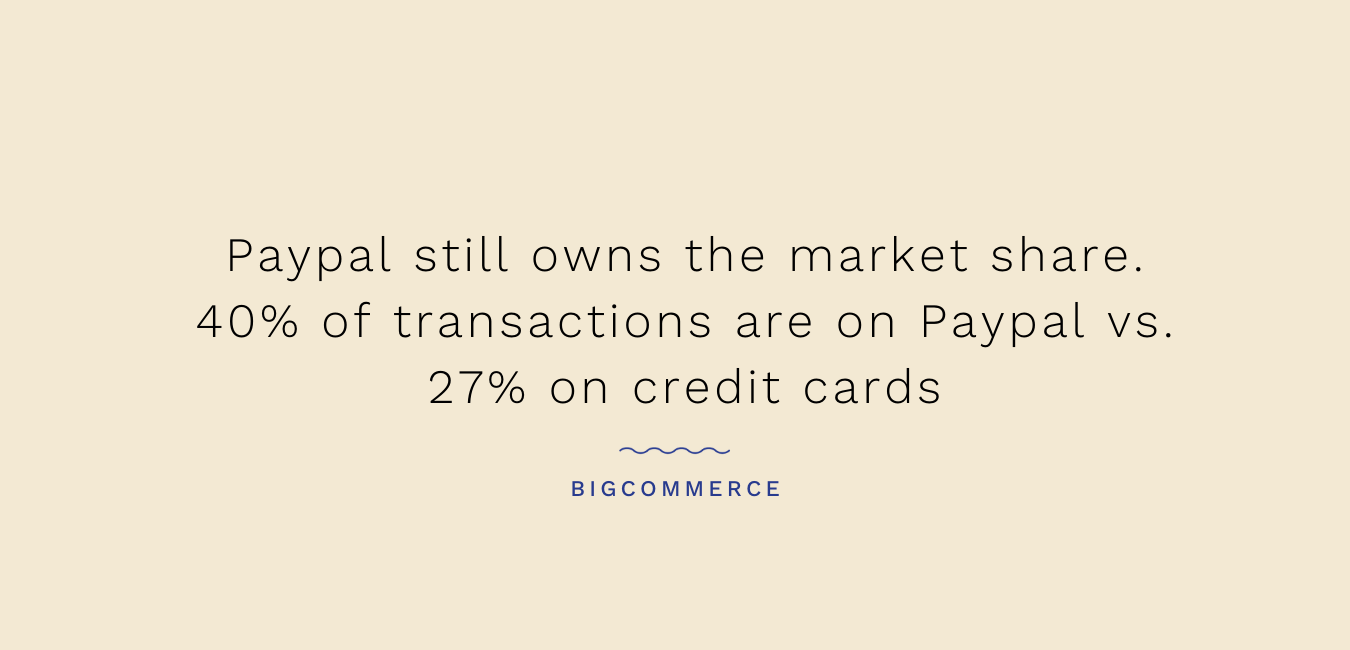

Despite the growth in BNPL, Paypal still owns the market share with 40% of all online transactions. Credit cards making up just 27%. (This one surprised me!)

-

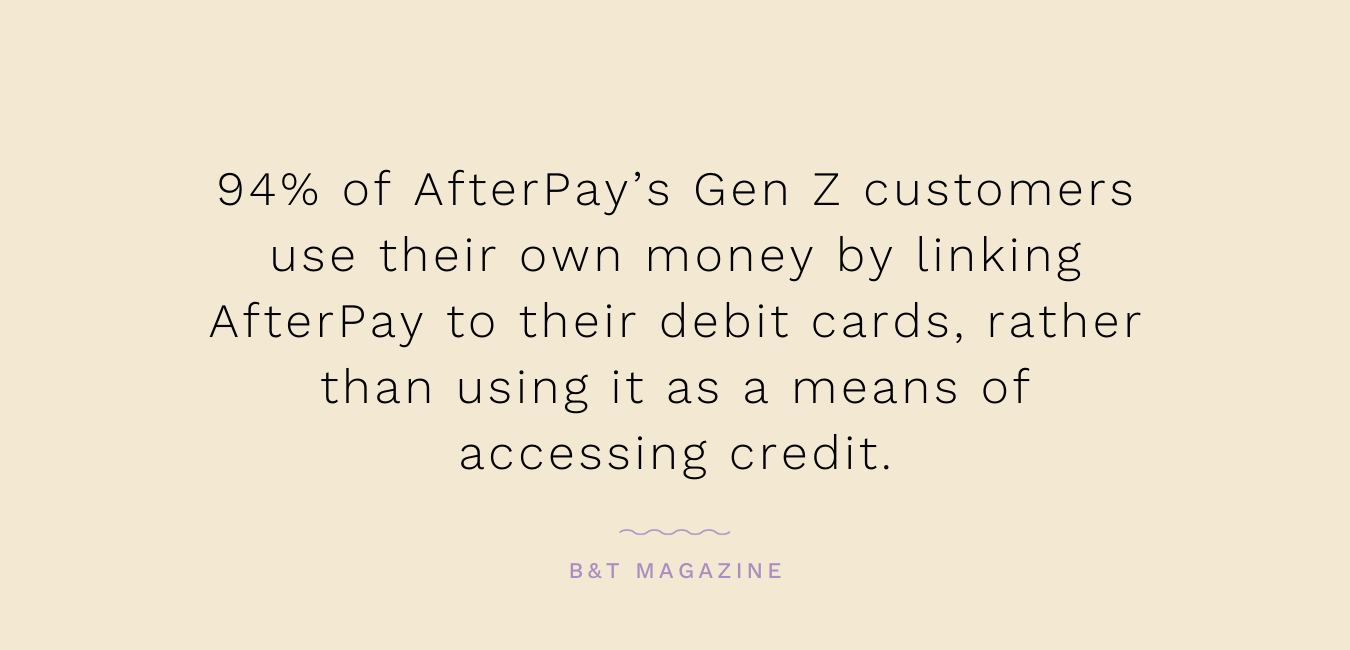

A whopping 94% of AfterPay’s Gen Z customers (currently 5 – 25 year olds) use their own money by linking AfterPay to their debit cards rather than using it as a means of accessing credit.

-

Unlike credit cards, Afterpay makes 85% of its money from its merchants fees, not its customers racking up interest. (Not so great for us business owners!)

Australian Buy Now Pay Later Providers

So as I’m sure you can imagine there are new BNPL providers popping up all the time, just a few right now are: AfterPay, Zip OpenPay, Humm, Payright, Klarna, Bundll and Limepay.

But what do you need to be considering as an e-commerce business owner?

-

Market share.

Who has the most users in your market (spoiler alert: probably AfterPay). People don’t like change so if we’ve already convinced a loyal tribe to use one provider the likelihood is this is what they’re going to reach for. The different providers also have majority share in different market sectors – e.g. Humm which may have more customers in the home improvement market than Zip.

-

Integration with your existing systems.

If your BNPL provider doesn’t integrate with your online POS then it’s going to make for a clunky user experience and likely fail to drive conversions.

Hot tip: Squarespace doesn’t currently support AfterPay through it’s commerce platform and doesn’t currently have it on their roadmap to support it. A massive red flag if you’re thinking about starting an e-commerce business on Squarespace.

-

Costs to you.

All these providers will charge you a transaction fee much like a credit card provider. However the fees for AfterPay for example are greater than most Credit Cards, so you want to weigh up if that is worth it for your business.

-

Future Trends

Instagram just released Reels, arguably the TikTok of Instagram. So even the big players will shake things up when a new kid arrives on the block and causes enough of a fuss. Keep your eyes on what’s happening and what’s new – just in case there are other providers that start to gain a competitive advantage on AfterPay.

OK, so tell me a bit about some of these BNPL companies.

The Big Guns

-

AfterPay

AfterPay is the market leader in Australia and almost as commonplace as a credit card option or Paypal when making a payment online.

But, want to know something wild?

I had never heard of it before moving to Australia.

AfterPay doesn’t have a global market share in the UK and Europe although it’s the lead BNPL provider in Australia, New Zealand, USA and Canada.

(If you’re interested, AfterPay only launched in the UK as Clearplay in June 2019.)

Although the fees to you as a business owner are more expensive than that of Credit Cards (and more expensive than Zip Pay) the incremental sales you’ll potentially see as a result of offering AfterPay (in my opinion) make it worthwhile. Personally, I think that if you’re going to run an e-commerce business in Australia right now you need to be offering AfterPay, regardless of whether or not you choose to also provide an alternative service. It’s something that consumers are looking for and want to use. I’d also argue that it’s great for your brand reputation to be associated with the kinds of brand partners that AfterPay currently offers. Your business might be different though.

-

Zip

For a while this Australian-owned BNPL provider was a bigger company than Coles!

Unlike AfterPay, ZipPay will complete a credit check before offering your customers their services. It’s fees are a little cheaper to you than with Afterpay. Both ZipPay and AfterPay are compatible with Shopify, WooCommerce and a couple of the other big players.

The New Kid on the Block: Klarna

So, Klarna was a thing back in the UK when I worked at ASOS, like waaay back when.

(Fun fact: It’s actually the only BNPL provider I’ve ever personally used.)

Klarna launched in Australia in January 2020 (wow, timing guys) and it’s still a little known underdog in the BNPL market here Down Under.

When I bang on about whether or not someone has Klarna it’s the one I usually get a response of ‘Huh?’ to.

But Klarna is one to watch out for as it’s got some serious clout in overseas markets and now it’s set its sights on the APAC market it’ll be interesting to see how it grows.

Klarna is a Swedish company and seen as one of the market leaders in some of the world’s most developed E-commerce markets in Europe and the UK. It has better usage coverage in the Global ecommerce market than AfterPay.

Here in Australia it’s backed by CBA and Australia Post commented back February that they are hoping to make Klarna available to their eCommerce merchants very soon (note: I’ve tried to see what became of this press release and… crickets. Anyone care to fill me in?)

Now tell me, will you be adding any of these other BNPL providers to your ecommerce business in the future?

Disclaimer: I cannot and do not provide any financial advice in relation to your business and the payment options that you may or may not choose to offer on your website. I do not take responsibility for any business decisions that you may choose to make as a result of reading this article.